How Infrastructure, Technology and Resources Are Quietly Redrawing the Global Order

Executive Summary

The classical map of geopolitics, once drawn by ideological borders and military alliances, is being overwritten by a rugged, material reality. Today, global supremacy is contested not merely through diplomatic consensus, but through the physical mastery of critical chokepoints: automated deep-water container ports, hyperscale data centers requiring gigawatts of power, rare-earth extraction facilities buried deep in the earth, and the ultra-clean cleanrooms where sub-three-nanometer silicon wafers are etched.

As the post-Cold War era of frictionless globalization gives way to an age of aggressive industrial policy and strategic reshoring, a new group of pivotal states is leveraging geography to redraw the global balance of power. This investigation traces the transformation of our global architecture across five interconnected battlefields—logistics, subsea infrastructure, artificial intelligence computing, critical mineral supply chains, and the emerging industrial corridors of the Atlantic and Global South—to map the true contours of the twenty-first-century empire.

The Mechanics of Friction

A Dispatch from the Mediterranean Rim

The Mediterranean mist at four o’clock in the morning carries the sharp, metallic tang of marine diesel and brine. From the observation deck of the control tower at Tanger Med, the world does not look like a borderless digital village; it looks like a colossal, hyper-automated machine.

Below, under the orange glow of towering sodium lamps, rows of automated rail-mounted gantry cranes move with the synchronized precision of an industrial ballet. They reach into the bellies of megaships—vessels longer than Eiffel Towers are tall—and pluck forty-foot steel containers from decks stacked twenty high.

To the north, across less than ten miles of black water, the lights of Gibraltar blink through the haze. Here, where Europe terminates and Africa begins, nearly twenty percent of all global maritime trade squeezes through a single geographical throat.

A decade ago, this stretch of Moroccan coastline was largely an expanse of sun-baked limestone cliffs and sleepy fishing villages. Today, it is the largest container port on the Mediterranean, an infrastructure behemoth handling millions of containers a year. It operates with a relentless, algorithmic rhythm. There are few humans visible on the tarmac. Instead, autonomous terminal tractors wheel between stacks, guided by local positioning networks and machine-learning software that calculates the most efficient route to shave fractions of a second off a ship’s turnaround time.

If you want to understand the fractured nature of the modern global economy, this is where you begin. For thirty years, the prevailing consensus among the global elite was that geography was dying. The internet, the World Trade Organization, and just-in-time logistics chains were supposed to have flattened the earth. Capital would flow wherever labor was cheapest; software would dissolve national sovereignty; distance would yield to efficiency.

That consensus has shattered. The world has discovered that the global economy is not a cloud; it is a physical circuit. It is built on concrete, copper, silicon, and steel. It is vulnerable to blockages, storms, political blockades, and missile strikes. The soft power of treaties and international institutions is rapidly being supplanted by the hard power of physical assets. From the deep-water docks of the Strait of Gibraltar to the cleanrooms of Taiwan, from the lithium flats of the Atacama Desert to the humming server halls of Virginia, a new map is being drawn. It is the geography of power, and it is being claimed by those who control the physical architecture of tomorrow.

The Tangible State

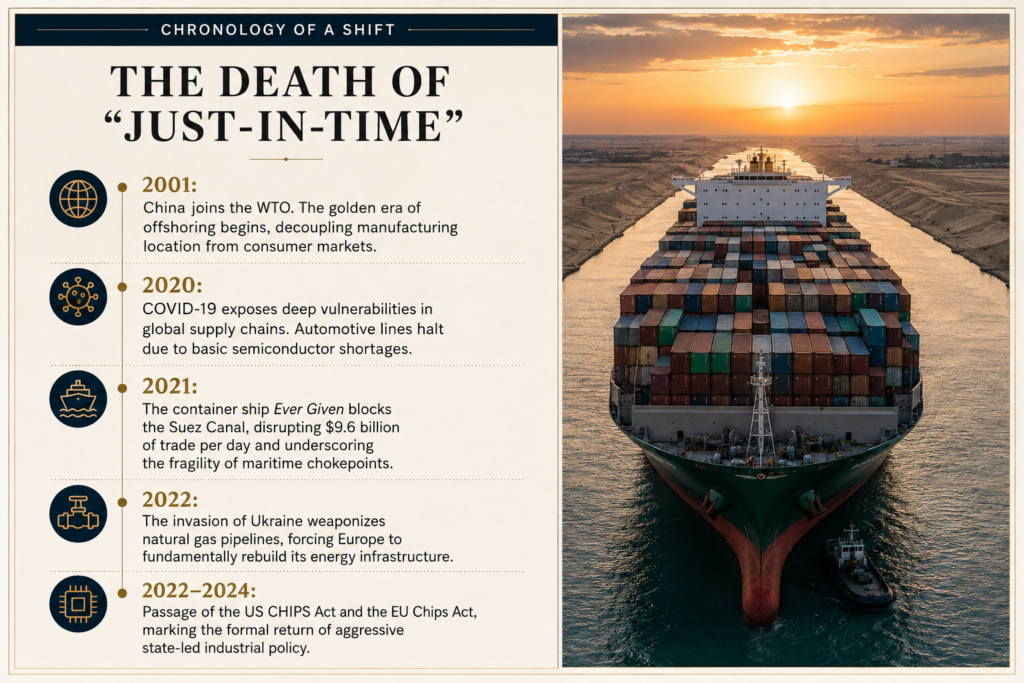

The Sudden Death of the Borderless Illusion and the Return of Industrial Geopolitics

For a generation, Western capitals operated on a comfortable philosophy: design in California or Munich, manufacture in Shenzhen, assemble across Southeast Asia, and consume everywhere. This was the gospel of the corporate supply chain, driven by a single-minded devotion to cost optimization. It produced cheap electronics, affordable automobiles, and historic corporate profits. But it also built a world of extreme systemic fragility.

The vulnerabilities of this hyper-globalized model became glaringly apparent over the last few years. A single massive container ship wedged sideways in the Suez Canal could paralyze ten percent of global commerce for days. A microscopic virus could shutter factories across five continents, leaving hospitals without basic medical supplies and automotive assembly lines frozen for lack of ten-dollar microchips.

“We built an economic system on the assumption that the weather would always be calm, the seas always open, and national governments always cooperative. It was an intellectual failure born of historic privilege. Now, the state is back, and it has brought its wallet.”

— Dr. Elena Rostova, Industrial Economist at the Center for Geoeconomic Strategy

The result is the dramatic return of industrial policy—a tool once dismissed by Western economists as an outdated relic of the mid-twentieth century. Governments are no longer content to let markets dictate where vital goods are produced. Today, the state is actively intervening, using hundreds of billions of dollars in subsidies, tax incentives, and domestic content requirements to drag manufacturing back within its own borders or into allied territories.

This is not traditional protectionism; it is something more complex: a doctrine of strategic resilience. The United States has unleashed trillions of dollars through historic legislative acts, seeking to rebuild its domestic semiconductor base and corner the market on clean energy technologies. The European Union has responded with its own Green Deal Industrial Plan and European Chips Act, aiming to double its share of global semiconductor production. China, through its long-running domestic initiatives and the multi-decade investments of the Belt and Road Initiative, continues to sink trillions into securing the raw materials and processing infrastructure of the Global South.

This scramble is creating a highly fragmented landscape. The old model of globalization valued efficiency above all else. The new model values security, redundancy, and alignment. Companies are moving away from “offshoring” to “nearshoring” (bringing production closer to home) and “friendshoring” (restricting supply chains to nations with shared values or strategic treaties).

This shift is creating entirely new winners and losers. Countries that find themselves on the right side of these new industrial corridors are experiencing unprecedented investment booms. Those that remain overly dependent on singular, vulnerable transport links or politically volatile trading partners face structural decline. The global economic architecture is being re-engineered, and its new foundations are deeply physical.

The Nervous System of Empires

The Hidden Vulnerabilities of Ocean Depths and Maritime Throats

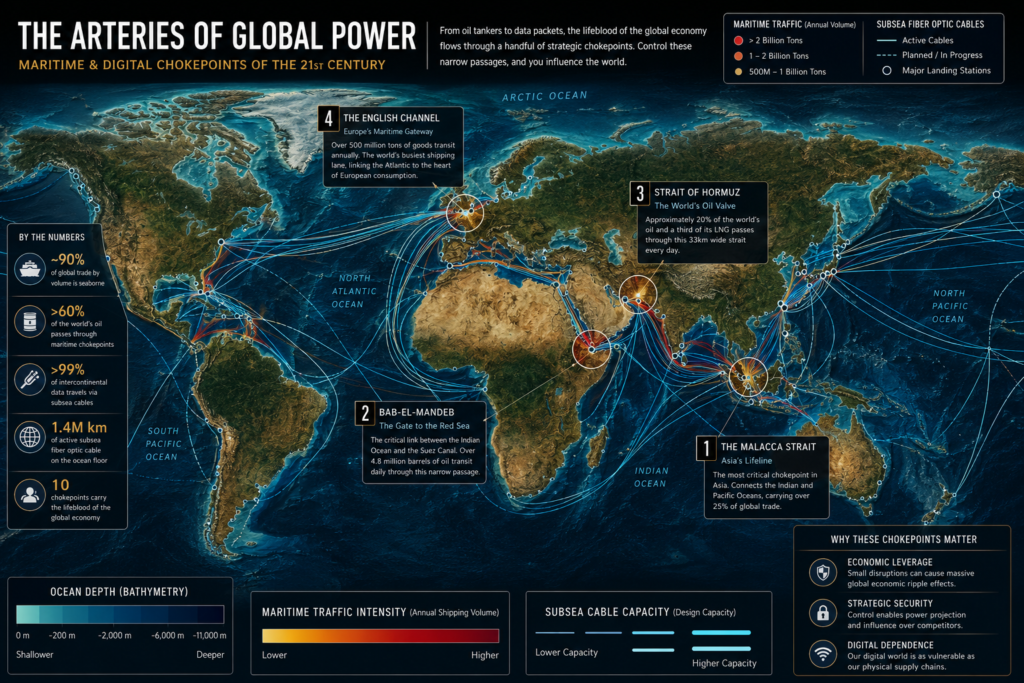

To understand how power is exerted today, one must look below the surface—literally. While the public eye focuses on satellite constellations and wireless 5G networks, the actual fabric of international communication is surprisingly physical, fragile, and bound by geography.

Consider the subsea fiber-optic cable network. More than 99 percent of all intercontinental data traffic travels through a web of underwater cables lying on the ocean floor, some no thicker than a garden hose. These cables are the nervous system of the global financial, corporate, and military apparatus. If you execute a high-frequency trade in London that clears in New York, or if a military drone in the Middle East is guided from an airbase in Nevada, that data flows through these deep-sea conduits.

But these cables do not cross the oceans at random. Because of maritime geography, they converge in narrow corridors, creating profound digital chokepoints. One of the most critical of these corridors runs through the Red Sea, across the narrow landmass of Egypt, and into the Mediterranean. Nearly a third of all internet traffic between Europe and Asia passes through this single, geographically constrained pathway. A well-placed anchor, an undersea earthquake, or a deliberate act of sabotage in this zone could instantly sever communication between two of the world’s largest economic blocs.

Editor’s Note

The reporting for this chapter involved interviews with subsea engineers, maritime security experts, and port operators across three continents. It underscores a fundamental truth of our era: the digital economy is entirely hostage to its physical infrastructure.

The physical vulnerability of these assets has transformed them into prime targets for geopolitical gray-zone warfare. Naval strategists no longer just look at surface combatants; they map the movements of specialized deep-sea research vessels equipped with autonomous underwater vehicles capable of splicing, tapping, or cutting cables miles beneath the surface. The destruction of major pipeline systems in Europe demonstrated that critical energy infrastructure on the seabed is highly vulnerable to deniable attacks.

The same dynamics govern the physical flow of commodities. While modern containerization has made shipping incredibly cheap, it has concentrated global trade into a handful of maritime gates: the Strait of Malacca, through which a quarter of all global oil and manufactured goods pass; the Strait of Hormuz, the artery for Middle Eastern crude; and the Panama Canal, which is increasingly vulnerable to climate-driven freshwater shortages that severely limit ship transits.

These chokepoints mean that maritime power is not an artifact of the nineteenth-century British Empire; it remains the ultimate arbiter of global stability. Whoever commands the seas, or possesses the engineering capability to build alternative routes around these bottlenecks, holds an effective veto over the global economy.

The Weight of the Mind

The Power Demands and Micro-Frontiers of Artificial Intelligence

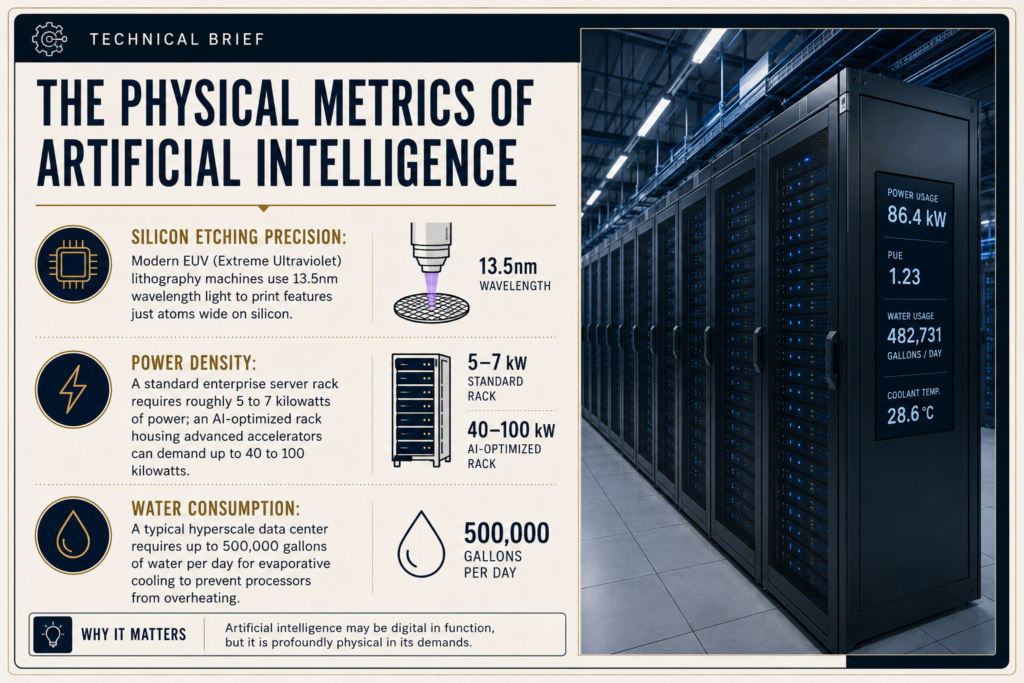

The prevailing myth of the digital revolution is that it is weightless. We speak of the “cloud,” of “virtual reality,” and of “artificial intelligence” as if they exist in a disembodied, ethereal realm. But artificial intelligence has a physical body, and it is ravenous.

To build and train a modern large language model requires thousands of specialized graphics processing units (GPUs) packed into warehouse-sized data centers. These facilities are among the most power-dense structures ever built. A single state-of-the-art hyperscale data center can consume as much electricity as a medium-sized city. By some estimates, the aggregate electricity demand of global data centers could double by the end of the decade, driven almost entirely by the computational demands of AI training and inference.

This reality has touched off a silent but desperate global race for two resources: advanced semiconductors and raw electrical power.

The semiconductor supply chain is perhaps the most complex and geographically concentrated manufacturing pipeline in human history. At its apex sit machines that use extreme ultraviolet (EUV) lithography to print features just atoms wide onto silicon wafers. These machines are manufactured by a single company in the Netherlands, ASML. They require components from hundreds of global suppliers—German lenses, American laser sources, Japanese chemical resists—and take months to assemble.

The wafers printed by these machines are then shipped to Taiwan, where advanced fabrication plants produce the actual silicon chips. A single facility can manufacture the vast majority of the world’s advanced processors. If that specific region were to experience a major seismic event or a geopolitical blockade, the global tech economy would come to a sudden halt.

“The true currency of twenty-first-century sovereignty is not gold, or even fiat currency. It is the control of compute.”

But even if you secure the chips, you still need to plug them in. In the United States, the traditional tech hubs like Northern Virginia—the data center capital of the world—are facing acute grid capacity constraints. Local utilities are warning that they cannot keep up with the exponential surge in demand from new AI facilities.

As a result, tech giants are scouring the globe for regions that can offer two things simultaneously: abundant land and secure, continuous electricity. This search is driving an unprecedented alignment between the tech sector and the energy industry. Companies are signing multi-decade power purchase agreements with nuclear plants, investing heavily in geothermal energy, and looking toward regions with rich renewable resources that can be tapped to power the next generation of intelligence.

The Periodic Table Trade Wars

How Critical Minerals Are Replacing Liquid Hydrocarbons

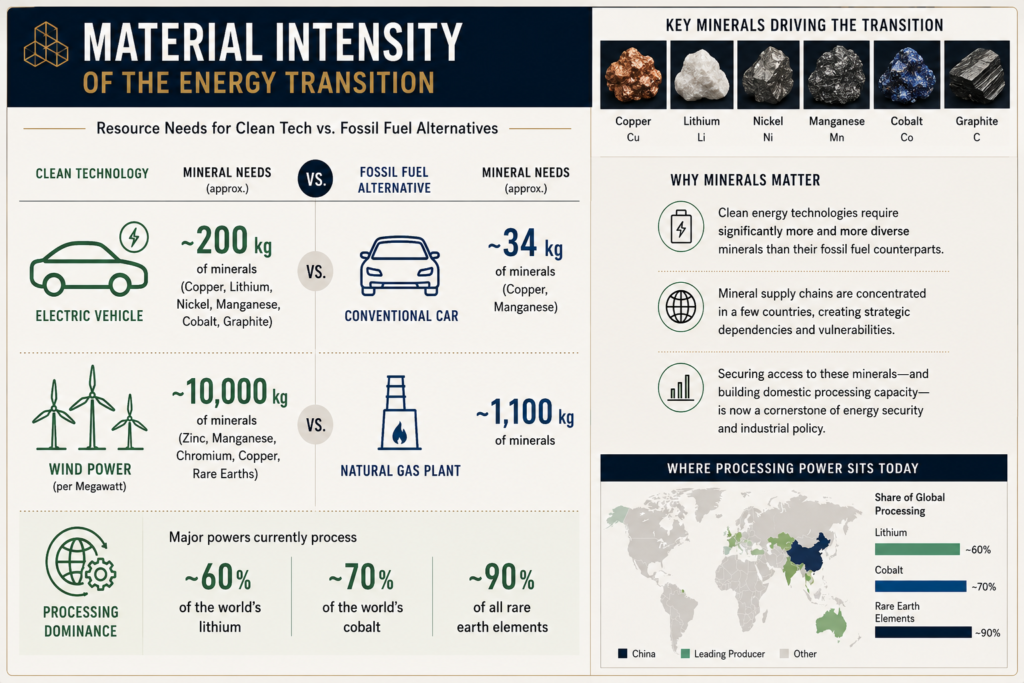

If the geopolitical battles of the twentieth century were fought over the liquid hydrocarbons of the Middle East, the conflicts of the twenty-first will be fought over the solid elements of the periodic table.

The global transition toward a low-carbon economy—electric vehicles, wind turbines, solar arrays, grid-scale storage batteries—requires an astronomical volume of minerals. A typical electric vehicle requires six times the mineral inputs of a conventional internal combustion engine car. An onshore wind plant requires nine times more mineral resources than a gas-fired plant of equal capacity.

We are moving from an energy system intensive in fuel to one intensive in materials.

The challenge is not necessarily that these materials are scarce in the earth’s crust. The challenge is that their extraction and, crucially, their processing are concentrated in a handful of geographies.

Take lithium, the essential ingredient in modern battery chemistry. The vast majority of the world’s extractable reserves are located in the “Lithium Triangle”—an arid high-altitude region spanning the borders of Chile, Argentina, and Bolivia—and in the hard-rock mines of Australia. Cobalt, critical for battery stability, comes overwhelmingly from Central Africa, where extraction is frequently plagued by severe socio-political challenges and systemic instability.

Yet, mining is only the first step. The true geopolitical bottleneck lies in the refining stage. It is here that specific Asian markets have spent three decades executing a brilliant, long-range industrial strategy. Through massive state subsidies, targeted investments, and consistent policy focus, they built a near-monopoly on the midstream processing of critical minerals.

Even when minerals are mined elsewhere, they are almost invariably shipped across ocean routes to be chemically purified into battery-grade materials.

Expert Insight

“The West is waking up to the reality that it cannot build a green domestic economy without relying on an incredibly concentrated supply chain. Breaking that monopoly will take decades of capital investment and a tolerance for domestic mining that many electorates simply do not possess.”

— Marcus Vance, Director of the Resource Security Initiative

This vulnerability has forced a frantic search for new mineral frontiers. Western mining companies and sovereign wealth funds are eyeing deposits across Africa, Latin America, and parts of Europe and North America. But opening a new mine is a notoriously slow process, often taking between ten and fifteen years from initial discovery to commercial production due to permitting, environmental reviews, and infrastructure development. The mismatch between rapid political targets for decarbonization and the slow reality of mining engineering is the central friction point of modern economics.

The Atlantic Pivot

Morocco’s Strategic Ascent as a Transatlantic and Decarbonized Node

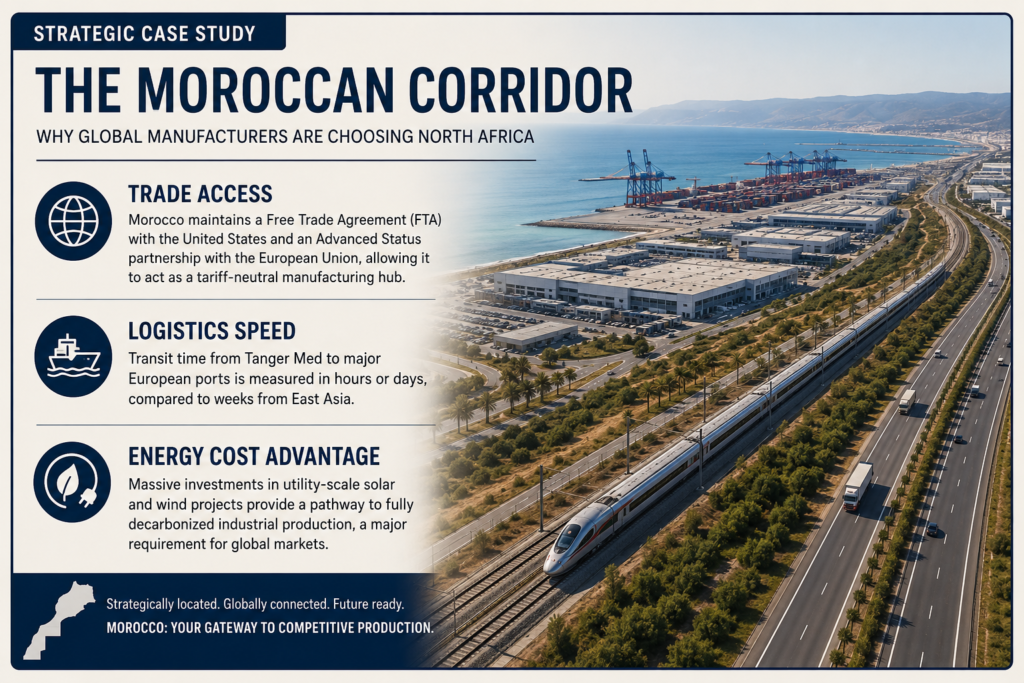

As the global supply chain fractures along lines of alliance and proximity, certain geographic nodes are quietly emerging as indispensable bridges. Among these, few are positioned as strategically as Morocco.

Historically seen as a bridge between Europe and Africa, the Kingdom is rapidly transforming into a major industrial and logistics hub for the new Atlantic economy. This evolution is no accident; it is the result of a deliberate, decades-long infrastructure strategy designed to leverage its unique geography at the western gateway to the Mediterranean.

The cornerstone of this strategy is Tanger Med, but its implications extend far beyond shipping containers. The port has acted as a catalyst for a massive domestic manufacturing ecosystem. Today, northern Morocco is home to one of the fastest-growing automotive clusters in the world. Leading global automotive corporations operate massive, highly productive assembly plants here, fed by hundreds of specialized tier-one and tier-two component suppliers. The country has become a dominant exporter of passenger cars, sending hundreds of thousands of vehicles across the Mediterranean to Europe every year.

But the country’s real geopolitical leverage in the new geography of power lies at the intersection of two critical fields: green energy and agriculture.

Morocco possesses some of the world’s largest reserves of phosphate rock, an essential ingredient in synthetic fertilizers. In an era of growing population and climate-induced food insecurity, phosphate is a strategic asset on par with oil. Crucially, the future of the battery industry is shifting toward Lithium Iron Phosphate (LFP) chemistry, which is cheaper and more stable than traditional nickel-cobalt formulations.

This has turned the nation into a magnet for battery manufacturers. Global firms are pouring billions into building cathode material and battery components facilities within Moroccan industrial zones, aiming to export directly to European and American markets under existing free trade frameworks.

Furthermore, the country is positioned to become a major exporter of green energy. With vast, sun-drenched expanses in the south and reliable coastal winds, it boasts some of the lowest production costs for solar and wind power globally. The Kingdom is leveraging this advantage to develop a domestic green hydrogen industry, with long-term plans to explore subsea pipelines and transmission cables to pump clean energy directly into the power-hungry grids of southern Europe.

This economic model represents a new form of diplomatic positioning. By remaining open to multi-directional investments while maintaining deep security and trade ties with Western capitals, Rabat has made itself an indispensable node in the fractured geography of globalization. It is a prime example of a “connector state”—a country that uses its physical location and sophisticated infrastructure to bridge the growing divides between the world’s major power blocs.

The Master Builders

Industrial Capacity, Sovereignty, and the Race for the Material Future

The re-shoring of industries, the scramble for critical minerals, the thirst for energy to power AI, and the hardening of maritime chokepoints are all symptoms of a larger, systemic shift. We are witnessing the end of the post-Cold War international order. The future will not be governed by a singular, rules-based global market, but by a competitive multi-polar system where power is directly tied to industrial capacity and physical resilience.

In this new era, the traditional definitions of power are being inverted. For decades, Western nations outsourced their industrial bases, believing that the high-value work lay in finance, software, and brand management. Manufacturing was treated as low-margin grunt work that could be safely delegated to developing countries.

This was an illusion. When a crisis hits, you cannot fight a pandemic with financial derivatives, nor can you secure an energy transition with software algorithms. You need factories. You need mines. You need engineers who understand how to bend metal, mix chemicals, and stabilize electrical grids.

The nations that dominate the coming decades will be those that master these physical disciplines. It will require a profound cultural and economic reorientation. Governments will need to find ways to train a new generation of skilled workers, rebuild domestic supply networks, and streamline the regulatory processes that currently make building infrastructure in legacy economies painfully slow and expensive.

At the same time, this physical scramble is happening against the backdrop of a changing climate. The irony is that the very tools we need to combat climate change—solar panels, wind turbines, electric grids—require an extraction and manufacturing apparatus that is itself highly vulnerable to extreme weather, water scarcity, and ecological disruption. The geography of power is inextricably linked to the geography of our changing planet.

The Enduring Ground

The late afternoon sun turns the Atlantic horizon into a sheet of beaten gold. From the cliffs above Tangier, you can watch the container ships head west out into the open ocean, destined for the ports of New York, Savannah, and Santos. They carry the physical wealth of nations, moving along routes that have remained virtually unchanged for centuries.

We have spent decades building an intellectual world that tried to escape the constraints of our planet. We believed that digital connectivity would render borders obsolete, that financial sophistication could replace material production, and that the cloud would liberate us from the mud.

It was a beautiful, brief delusion. But geography has returned, with a vengeance. It reminds us that our societies are held together not by the lines of code on our screens, but by the steel cables on the ocean floor, the high-voltage lines that hum over our heads, and the deep-water docks that receive the ships. The empire of software is ultimately hostage to the kingdom of stone. As the clouds of ideological conflict gather once more across the world, the nations that endure will be those that remember a foundational truth of human civilization: the future is not something you download; it is something you build.