Why the world still runs on a currency it complains about

Every few years, the dollar is declared to be dying. The complaints are real, the grievances are legitimate, and the exits keep being announced. And every few years the world does the same thing it did the year before: when something breaks — a war, a pandemic, a banking panic — it runs toward the dollar, not away from it. The paradox at the centre of the global economy is not that the dollar is weak. It is that the world resents the dollar and cannot quit it, and that the two facts have the same cause.

The Phrase That Started as an Insult

The term was coined in the 1960s, and it was not a compliment. Valéry Giscard d’Estaing, then France’s finance minister, used “exorbitant privilege” to describe something that offended him: the United States, alone among nations, could settle its debts to the rest of the world in a currency it alone could print. When France ran a deficit, it had to pay in gold or dollars it did not control. When America ran a deficit, it paid in dollars it created at will. Charles de Gaulle found this intolerable, and spent the decade demanding gold from Washington in exchange for France’s dollar holdings — a slow-motion run on Fort Knox that helped bring down the entire post-war monetary order in 1971.

Sixty years later, the privilege is intact, the resentment is global rather than merely French, and the mechanics have grown far stranger than Giscard could have imagined. Understanding what that privilege actually is — what it buys, what it costs, and why it has proved so impossible to dislodge — is the key to one of the central puzzles of the present moment: why a fractured, multipolar, America-sceptical world remains, in its plumbing, overwhelmingly dollarised.

Start with the size of the thing, because the numbers are genuinely difficult to absorb.

What the Privilege Actually Buys

Strip away the rhetoric and the exorbitant privilege resolves into three concrete advantages, each worth a great deal, and each carrying a hidden charge.

Cheap money, forever. The world needs dollars — to trade, to borrow, to hold in reserve — and the safest dollar asset is a US Treasury bond. So the world buys Treasuries, in enormous and reliable quantity, largely regardless of the yield on offer. That standing bid lets the American government borrow more cheaply than its finances alone would justify, and lets American households borrow cheaply too, because global demand for dollar assets flows through the whole system. Estimates vary, but the interest-rate discount is real and persistent. It is, in effect, a permanent subsidy paid by the rest of the world to American borrowers, in exchange for the safe, liquid asset only America supplies at scale.

The ultimate insurance. Because the dollar is what everyone runs toward in a crisis, the United States enjoys something no other country has: its borrowing costs tend to fall precisely when the world is on fire. In 2008 — a crisis made in America — global capital fled into US Treasuries. In March 2020 the same thing happened. This is the “exorbitant privilege” at its most vivid: the issuer of the world’s safe asset is insured by the very panics it may have caused.

The financial weapon. This is the newest and most consequential. Because dollar payments ultimately clear through American banks and American infrastructure, Washington can exclude a target from the dollar system — and therefore from most of world trade — with a stroke of a pen. Sanctions on Iran, on North Korea, and above all the freezing of roughly $300 billion in Russian central-bank reserves in 2022 turned the privilege into an instrument of war. That episode is the single most important thing to happen to the dollar’s global position in a generation, and not in the way Washington’s critics assume.

Each advantage has a shadow. Cheap borrowing enables chronic deficits. The safe-haven bid can overvalue the currency and hollow out exporters. And the weapon, used often enough, teaches the world to build somewhere else to stand. Which brings us to the trap at the centre of the whole arrangement.

The issuer of the world’s safe asset is insured by the very panics it causes. That is the privilege — and, as we shall see, also the trap.

The paradox in a sentence.

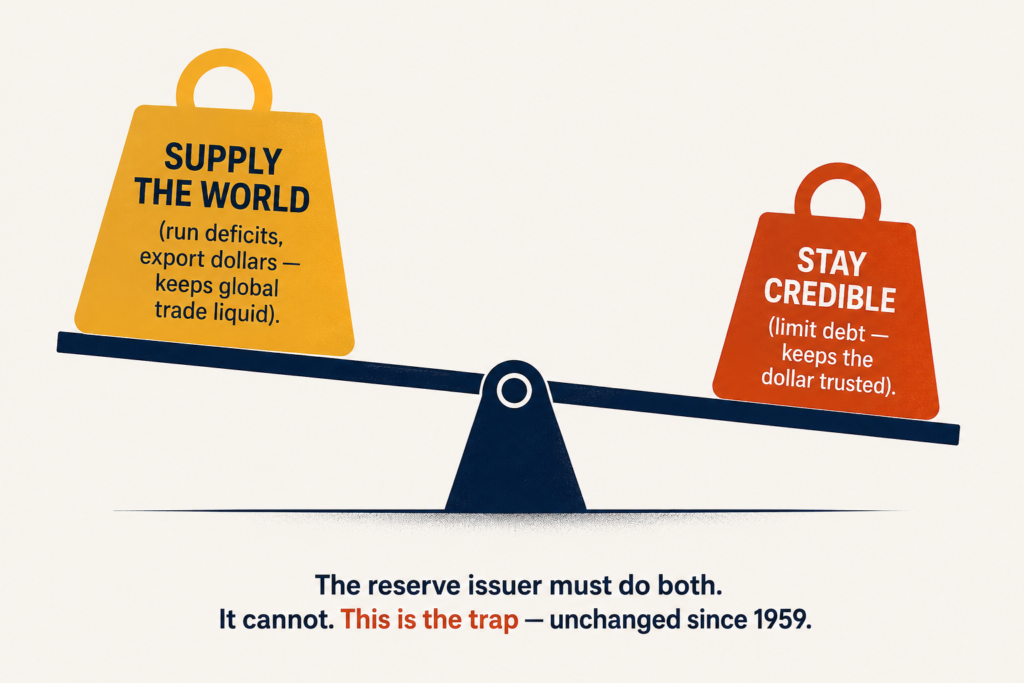

The Triffin Dilemma

In 1959, a Belgian-American economist named Robert Triffin testified before the US Congress and identified a contradiction that has never been solved, only managed. It is the intellectual heart of this entire subject, and it is worth stating carefully, because almost every argument about the dollar’s future is really an argument about Triffin.

The world needs the reserve currency to be abundant. For the dollar to lubricate global trade and satisfy the world’s demand for safe assets, the United States must supply dollars to everyone else — and the way it does that is by running persistent deficits, sending out more dollars than it takes back. The rest of the world’s reserves are, quite literally, America’s deficits held abroad.

But the world also needs the reserve currency to be sound. Confidence in the dollar depends on the belief that it will hold its value and that America’s obligations remain credible. And a country running ever-larger deficits, issuing ever more debt, is a country whose soundness is eventually called into question.

There is the trap. To supply the world’s reserve asset, you must behave in a way that gradually undermines confidence in that same asset. Provide too few dollars and you strangle global trade and liquidity. Provide too many and you erode faith in the currency. The reserve issuer is required, structurally, to do both the thing that sustains the system and the thing that corrodes it — at the same time, forever.

Triffin predicted this would sink the gold-backed Bretton Woods system, and in 1971 it did: the United States had issued far more dollars than it held gold to redeem, de Gaulle and others came to collect, and Richard Nixon closed the gold window rather than empty the vaults. What replaced it — pure fiat dollars, backed by nothing but the depth of American markets and the credibility of American institutions — did not resolve Triffin’s dilemma. It simply removed the hard constraint of gold, allowing the contradiction to run further and longer than Triffin imagined possible. It is still running today. Every warning about unsustainable US debt, and every reassurance about America’s unique capacity to carry it, is a restatement of the same 1959 insight.

The Great De-Dollarisation, Measured

Now to the claim you have heard a hundred times: that the world is abandoning the dollar. It contains a truth wrapped in an exaggeration, and separating them is the most useful thing this article can do.

The truth first. The dollar’s share of allocated global reserves has genuinely fallen — from more than 70% in 2000 to roughly 57% by 2025. Central banks are, deliberately and measurably, diversifying. This is not imaginary, and the people who dismiss de-dollarisation entirely are as wrong as the people who predict imminent collapse.

Now the exaggeration, in three parts.

First: much of the “decline” is an optical illusion of accounting. Reserves are measured in dollars. When the euro or the yen rises against the dollar, the dollar value of everyone’s euro and yen holdings goes up — and the dollar’s share mechanically falls, even though no central bank sold a single dollar. The IMF itself has stressed that once you adjust for these exchange-rate movements, the dollar’s reserve share in recent quarters has been close to flat. A meaningful part of the widely reported “flight from the dollar” is arithmetic, not action.

Second: the money leaving the dollar is not going where the headlines suggest. It is not flowing into the renminbi, whose reserve share sits around 2% and has been flat to falling for three years. It is trickling into a scattering of smaller “non-traditional” currencies — the Australian and Canadian dollars, the Korean won, the Singapore dollar — and, above all, into gold. Central banks bought more than a thousand tonnes of gold a year for three consecutive years, and the single clearest trigger was the freezing of Russia’s reserves. The lesson every non-aligned central bank drew in 2022 was not “buy yuan.” It was: buy the one reserve asset that no foreign government can freeze. Gold has no issuer, no jurisdiction, and no off switch.

Third: reserves are the slow-moving part. The dollar’s grip is tightest exactly where it is hardest to see — in the plumbing. Around 88% of currency trades, roughly half of trade invoicing, the overwhelming majority of cross-border bank lending, and the pricing of most globally traded commodities still run on dollars. You can diversify your reserve portfolio in an afternoon. You cannot re-plumb the invoicing of world trade, the denomination of global debt and the architecture of correspondent banking in anything less than decades — and only if something better exists to move to.

Which raises the question the whole debate turns on. If not the dollar — then what?

Why the Yuan Cannot (Yet) Do It

China has the world’s second-largest economy, its largest manufacturing base, its largest trading network, and an explicit ambition to internationalise its currency. It has built an alternative payments system, CIPS, to route around Western infrastructure. On paper, the renminbi is the obvious challenger. In practice, it is stuck at around 2% of global reserves, and the reason is not a conspiracy or a failure of ambition. It is a contradiction Beijing has chosen not to resolve.

A reserve currency requires something China does not want to provide: an open capital account. To hold your currency in reserve, the world must be able to move large sums in and out freely, buy and sell your government bonds without permission, and trust that their money is not trapped by capital controls or seized on a political whim. A true reserve currency is a promise of unconditional access to a deep, open, liquid financial market governed by predictable rules.

China’s entire economic model runs the other way. Capital controls are not an oversight Beijing has failed to remove; they are a core instrument of state power, used to manage the exchange rate, direct credit, prevent capital flight and preserve the Communist Party’s control over the financial system. Opening the capital account fully would mean surrendering much of that control and accepting the possibility of destabilising outflows — exactly the loss of control the Party exists to prevent.

This is China’s own Triffin dilemma, in a harsher form. To make the renminbi a global reserve currency, China would have to run current-account deficits — supplying renminbi to the world — and open its financial markets completely. Both cut against the deepest priorities of the Chinese state: its export-led growth model and its political control over capital. Beijing wants the prestige and the sanctions-resistance of a reserve currency without paying the price of monetary openness. That is not available. There is no reserve currency without an open capital account, and there is no open capital account without a loss of control that China has repeatedly, deliberately, declined to accept.

So the renminbi grows where it can — in bilateral trade with China, in settling Russian oil, in the accounts of countries under Western sanctions with nowhere else to go — and stalls where it cannot. It is becoming a currency of necessity for a bloc, not a currency of choice for the world. Those are very different things, and only one of them replaces the dollar.

There is no reserve currency without an open capital account — and no open capital account without a loss of control that Beijing has repeatedly declined to accept.

Why the obvious challenger isn’t one, yet.

What a Multipolar Money World Actually Looks Like

Here is where the honest analysis parts company with both camps — the dollar-collapse camp and the dollar-forever camp. The likeliest future is neither replacement nor permanence. It is fragmentation: a world that does not switch currencies so much as split into overlapping zones, held together at the centre by a dollar that is weaker than it was and still without a peer.

Picture it not as a throne changing hands but as a core-and-blocs arrangement. At the core, the dollar remains the primary global reserve, the main invoicing currency for commodities and cross-border finance, and the safe asset of last resort — diminished from its peak, resented, but unreplaced, because the alternatives each fail a different test. The euro is deep and open but lacks a unified fiscal backbone and a single safe asset to rival the Treasury market. The renminbi is large but closed. Gold is sovereign-proof but cannot be lent, priced or scaled as the working currency of trade.

Around that core, blocs harden. A renminbi zone for trade with China and for states frozen out of the dollar system. Bilateral local-currency arrangements — India paying for Russian oil in rupees and dirhams, Brazil and China settling some trade directly — that chip at the edges without touching the core. And running underneath all of it, gold as the neutral reserve asset of a low-trust world: the thing you hold precisely because it answers to no one.

This is a messier, more expensive, more fragmented monetary order than the one that prevailed after 1991. It has more friction, more currency risk, more parallel plumbing. It is less efficient for everyone, including the United States, whose privilege slowly erodes at the margin. But it is not a world with a new king. It is a world with a weakened one and no successor — which is a different, and more unstable, thing than the clean multipolarity that both Beijing and the dollar’s obituarists like to imagine.

The irony is exquisite, and it is the note to end on. The single greatest accelerant of this fragmentation was not Chinese ambition or European integration. It was the American decision, in 2022, to weaponise the dollar against Russia — to prove, definitively, that dollar reserves can be switched off. That act did more to convince the world’s central banks to diversify than a decade of Beijing’s speeches. The privilege, used as a weapon, taught the world to fear the weapon and to arm against it.

The Currency the World Cannot Quit

Return to the paradox with which we began. The world complains about the dollar — legitimately. It resents the exorbitant privilege, the subsidised deficits, the extraterritorial reach of American law, the ever-present possibility of being cut off. Every one of these grievances is real, and the drive to build alternatives is a rational response to them.

And yet, when the next crisis comes — and one always comes — the same central banks that spent the previous year diversifying will do what they have done in every crisis of the modern era: they will scramble for dollars. Because in the moment that matters, the question is never “which currency do I resent least?” It is “what can I sell, right now, at size, to anyone, without asking permission?” And the answer, for now and for some time yet, is the thing the whole world claims to be leaving.

The dollar’s dominance does not rest on affection, or on trust in American wisdom, or even on the strength of the American economy. It rests on a network effect so deep that leaving requires not just a decision but a coordinated global reconstruction that no one can lead and no one can finance. Everyone uses the dollar because everyone uses the dollar. That is a tautology, and it is also the single most powerful force in international finance.

Giscard called it exorbitant, and he was right. What he did not see — what de Gaulle, demanding his gold, did not see — is how much more exorbitant a privilege becomes when it is woven so deeply into the world’s plumbing that even the countries trying hardest to escape it must use it to build the exits.

The dollar is not loved. It is not trusted. It is not even, by the standard measures, entirely sound. It is merely indispensable — and indispensability, it turns out, is worth more than all three.

The Numbers, and How Far to Trust Them

Dollar share of allocated reserves ~57% (Q3 2025); >70% in 2000. IMF COFER, the authoritative source; total allocated reserves ~$13 trillion. Confidence: high. Note the recurring caveat below on exchange-rate effects.

“Much of the recent decline is exchange-rate arithmetic, not selling.” The IMF’s own COFER commentary (Oct 2025) states the dollar’s share was roughly flat in Q2 2025 once adjusted for currency moves. Confidence: high — this is the IMF’s stated position, and it is the most under-reported fact in the whole debate.

~88% of FX transactions; ~half of trade invoicing. BIS Triennial Survey (FX turnover) and invoicing studies. Because each FX trade involves two currencies, shares sum to 200%, so 88% is near the structural maximum. Confidence: high.

Renminbi ~2% of reserves, flat-to-falling. IMF COFER, 2023–25. Confidence: high.

~$300 billion in Russian reserves frozen, 2022. Widely reported; some sources cite ~$320 billion including all jurisdictions, the largest tranche (~€194bn) in Belgium’s Euroclear. Freezing immobilised the assets; outright confiscation is a separate, later, still-contested step. Confidence: high on the freeze; medium on any figure for seizure — that story is live and the legal position keeps moving. Date-stamp it.

Central banks bought 1,000+ tonnes of gold a year, three years running. World Gold Council. 2025 figures are strong but some sources report a modest step-down from the 2023–24 peak; China’s true buying is widely believed to exceed its official reports, which is an estimate, not a fact. Confidence: high on the trend; medium on precise annual tonnage and on China’s unreported buying.

The Triffin dilemma and “exorbitant privilege.” Robert Triffin’s 1959–60 congressional testimony; the phrase is attributed to Valéry Giscard d’Estaing in the 1960s. Confidence: high — these are documented intellectual history, not contested data.

The borrowing-cost “subsidy.” That reserve status lowers US borrowing costs is well established; the precise size is genuinely disputed among economists (estimates range widely). Confidence: high on the existence of the effect; low on any single number — which is why the article gives none.

To Go Deeper

Eichengreen, B. (2011). Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System. Oxford University Press. The essential history, by the field’s leading authority.

Triffin, R. (1960). Gold and the Dollar Crisis: The Future of Convertibility. Yale University Press. The original statement of the dilemma — still startlingly current.

International Monetary Fund. Currency Composition of Official Foreign Exchange Reserves (COFER). The quarterly source of record; read the accompanying blog for the exchange-rate-adjustment caveat that most coverage omits.

Bank for International Settlements. Triennial Central Bank Survey of FX and OTC derivatives markets. The definitive picture of what actually trades, as opposed to what is held in reserve.